A Question of Equilibrium

"Sellers were out in force on the market today after negative news on the economy." It's a common line in TV finance reports. But have you ever wondered who is buying if so many people are selling?

The notion that sellers can outnumber buyers on down days doesn’t make sense. What the newscasters should say, of course, is that prices adjusted lower because would-be buyers weren’t prepared to pay the former price.

What happens in such a case is either the would-be sellers sit on their shares or prices quickly adjust to the point where supply and demand come into balance and transactions occur at a price that both buyers and sellers find mutually beneficial. Economists refer to this as equilibrium.

But the price at which equilibrium is reached can change. That’s because new information is coming into the marketplace continually, forcing would-be sellers and would-be buyers to constantly adjust their expectations.

That new information might be company-specific news on earnings. It might be news that has implications for specific industries—like a spike in oil prices. Or it might be an economic development that affects the entire market, like a change in the unemployment rate. Given this constant flux in the flow of news and information and the changing expectations of participants, it can be reassuring to remember that for everyone selling shares there must also be buyers of those shares—or the trade will never take place. And whenever information changes, prices may change and quickly reach a new level of equilibrium.

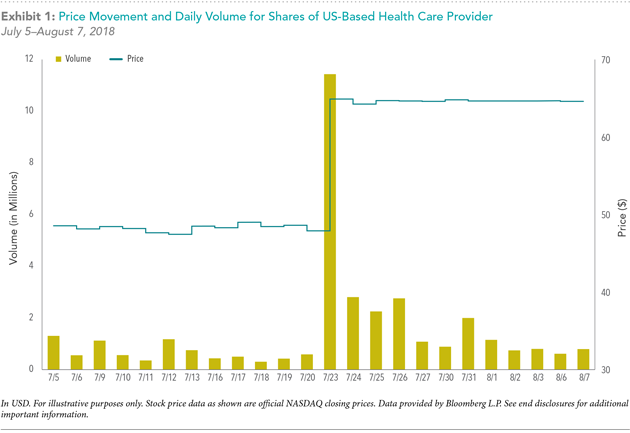

Recent trading activity by market participants in shares of a US-based health care provider offers a clear example of how quickly prices adjust to new information. It was reported in late July 2018 that a large private equity firm was in talks to purchase the health care firm at a price valuing the company at $65 per share. Prior to the announcement, shares of the firm were trading around $48. As we see in Exhibit 1, when the announcement broke, the market price for the stock adjusted overnight to just below $65. In other words, after news of the impending sale hit the market, the supply and demand for the stock met at a new equilibrium price.

Given that security prices rise and fall based on a multiplicity of influences, how should investors interpret and act on these signals? We believe that trying to untangle all these influences and profit from perceived mispricing is not possible in a systematic and scalable manner.

An alternative approach is to start by accepting that prices are fair and reflect the collective expectations of market participants. While information frequently changes, this is quickly built into prices. Competition among buyers and sellers is such that it’s not possible to consistently outguess the market.

The second step is to see that fairly priced securities can have different expected returns. And we can use market prices and security characteristics to identify those securities that offer higher expected returns.

The third step is to build highly diversified portfolios around these broad drivers of return, while implementing efficiently and managing the cost of buying and selling securities.

The final step is to apply discipline and rebalance your portfolio to either stay within your chosen risk parameters or to adjust for changes in circumstances.

Ultimately, the market is like a giant information processing machine. All the influences mentioned above are constantly being assessed by millions of participants, and prices adjust based on those collective expectations.

The returns we expect from investing do not necessarily show up every day, every week, every month, or even every year. But the longer we stay invested, the more likely we are to capture them. So, rest assured that even when prices are falling, people are still buying. The market is doing its job, and we believe the rewards will be there if you remain disciplined.