Planning Series: Insurance - "Just another expense?"

Everyone loves insurance, right? Especially those who pay insurance premiums year after year for no perceived/tangible gain. Yet in planning, insurance is too often ignored. It is common for clients to groan about purchasing more insurance; they would much rather talk about the client’s investment portfolio or the age they can afford to retire. Insurance is an important part of a comprehensive financial plan that Stowe Financial Planning evaluates for all its clients.

Consumers regularly debate if insurance coverage for a risk of some low probability event is worth the cost in insurance premiums they must pay. With investing, it makes sense; take on a certain amount of risk for a desired return. Evaluating the need for insurance is slightly more complicated than that. So how do you protect all current and future assets against possible risks of loss? The answer is proper use of risk management.

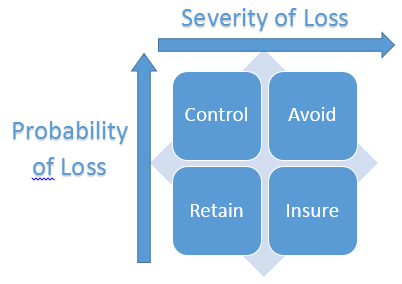

To make things easier, some risks may not need to be insured at all. Look at the diagram below.

For less severe losses, insurance would not be reasonable. You can manage or control risk by reducing the likelihood of loss. For example, you could add sand to your steps in icy weather, or install fire sprinklers at your workplace, or a security system in your home, or limit the cash you carry with you.

For high probability and high magnitude risks, the insurance company may not be willing to insure that risk. Even if they do, the premium charge would be expensive because of the additional risk the company takes on. The best solution is to avoid the risk completely. For instance, you might avoid buying a house in a flood plain, or refrain from driving on the highway, or not allow the kids to have a trampoline.

For low probability losses, the best solution to manage risk is to retain (self-insure) or transfer the risk to a third party (purchase insurance). It makes sense to self-insure for the rare and miniscule loss. Your financial well-being will not be affected by the small loss. Another way to retain risk is by selecting a higher deductible. You assume the additional risk of the higher deductible in exchange for lower premium costs. Retention of risk offers multiple advantages. If the actual losses do not exceed the amount paid in premiums, you would have been better off without insurance. By self-insuring, you have the opportunity to earn an investment return and still be able to recoup losses if need be.

Insurance is needed to protect against the unlikely catastrophic event or large expense that would be detrimental to your family. What if your child suddenly needs a heart transplant? Or you are severely injured at work? Even though the chance that an event like those would happen to you is quite low, the magnitude of wealth lost in those situations would dramatically affect your financial future.

When evaluating insurance options, remember these key points.

- Future earnings would be lost if something terrible happened to you or your spouse. Protect that income with life and disability insurance proceeds. If you made $50,000 after taxes each year and received a 3% annual increase, you would earn over $2.3 million over the next 30 years. Yet, it would be too costly to insure for a $2 million policy. A more sensible approach would be to purchase an appropriate level of coverage that maintains your family’s lifestyle.

- At some point in your lifetime, it is likely you will self-insure for life insurance. It is illogical to continue life insurance coverage after the kids have moved away or you age into your 60s. Plus, clients that have done sound financial planning can afford to self-insure because they have saved a sizeable nest egg to withdraw from. You no longer have a need for insurance because the risk no longer affects the financial plan.

- Do research yourself or consult an expert as the various types of insurance and complex terminology can be confusing. It is always a good idea to shop around and investigate the financial security of the insurer.

- Generally, avoid combining investments and insurance. The unnecessary expense of commissions and management fees hinder investment performance.

- A rule of thumb is to buy term life insurance, rather than the more costly whole life policy, and invest the difference in premiums. However, every family or individual is unique. Certain types of coverage may be excellent for some while for others would be senseless. As financial planners always say “It depends.”

Written by Roddy Warren

Issued November 12, 2014