How I Learned to Love the Bond, (at least short term bonds): Revisited

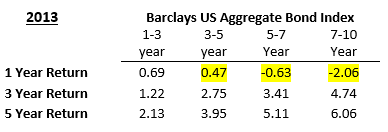

Earlier this year, I wrote a column discussing the abnormal bond environment and explaining why client’s bond allocations are largely located in low-yield, short-term bonds. In an ordinary interest rate environment, an investor expects to be compensated for the risk assumed with longer-term bonds. As you can see below, 2013 was not kind to intermediate (3-5 years) and long-term (5+ years) bonds.

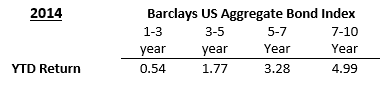

Just as we thought rates were going back to normal, rates dropped down again at the start of the new year. Longer bonds have generated exceptional returns so far this year (see in table below). Whereas, short-term bonds stayed about the same.

We achieved our goal with short-term bonds…stability. Consequently, stability is the same reason why client portfolios trail the bond index. But, we are okay with that. We are certain that the rise of interest rates is inevitable. Not if, but when. Then, intermediate and long-term bond prices will fall just like 2013 and we would be having a completely different conversation.

Since August 2012

Take a look at how the bond index (BIV - Vanguard Intermediate-Term Bond ETF) performed in the last two years compared to a common short-term bond fund we recommend (DFIHX - DFA One-Year Fixed-Income I). Until the market normalizes, we will continue to use DFIHX and other short-term bond funds. We believe the YTD bond performance is a temporary deviation from the long-run trend shown above. We are confident that our position will be vindicated in the next six to twelve months… the government cannot keep this charade of artificial rates up forever.

By Roddy Warren