Evidence-Based Investment Insights: Factors That Figure in Your Evidence-Based Portfolio

Welcome to the next installment in our series of Stowe Financial Planning’s Evidence-Based Investment Insights: Factors That Figure in Your Evidence-Based Portfolio.

In our last piece, “The Essence of Evidence-Based Investing” we explored what we mean by “evidence-based investing.” Grounding your investment strategy in rational methodology strengthens your ability to stay on course toward your financial goals, as we:

- Assess existing factors’ capacities to offer expected returns and diversification benefits

- Understand why such factors exist, so we can most effectively apply them

- Explore additional factors that may complement our structured approach

Assessing the Evidence (So Far)

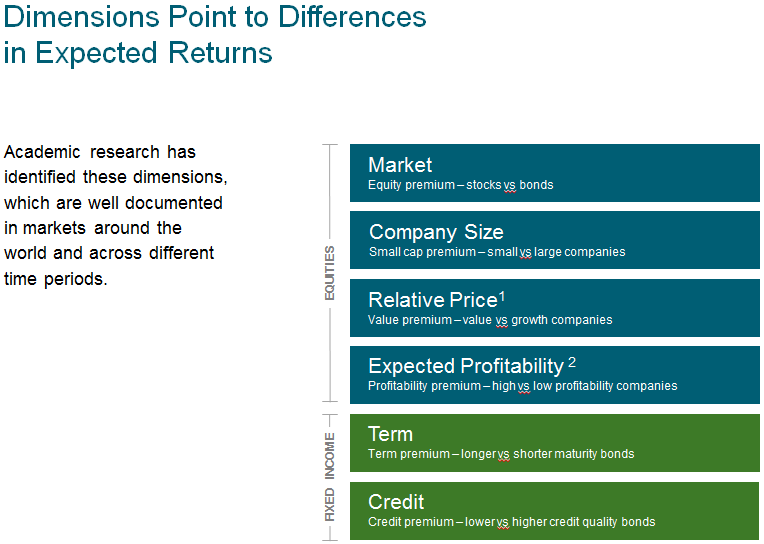

An accumulation of studies dating back to the 1950s through today has identified three stock market factors that have formed the backbone for evidence-based portfolio construction over the long-run:

- The equity premium – Stocks (equities) have returned more than bonds (fixed income), as we described in “What Drives Market Returns?”

- The small-cap premium – Small-company stocks have returned more than large-company stocks.

- The value premium – Value companies (with lower ratios between their stock price and various business metrics such as company earnings, sales and/or cash flow) have returned more than growth companies (with higher such ratios). These are stocks that, based on the empirical evidence, appear to be either undervalued or more fairly valued by the market, compared with their growth stock counterparts.

If you ever hear financial professionals talking about “three-factor modeling,” this is the trio involved. Similarly, academic inquiry has identified two primary factors driving fixed income (bond) returns:

- Term premium – Bonds with distant maturities or due dates have returned more than bonds that come due quickly.

- Credit premium – Bonds with lower credit ratings (such as “junk” bonds) have returned more than bonds with higher credit ratings (such as U.S. treasury bonds).

Understanding the Evidence

Scholars and practitioners alike strive to determine not only that various return factors exist, but why they exist. This helps us determine whether a factor is likely to persist (so we can build it into a long-term portfolio) or is more likely to disappear upon discovery.

Explanations for why persistent factors linger often fall into two broad categories: risk-related and behavioral.

A Tale of Risks and Expected Rewards

It appears that persistent premium returns are often explained by accepting market risk (the kind that cannot be diversified away) in exchange for expected reward.

For example, it’s presumed that value stocks are riskier than growth stocks. In “Do Value Stocks Outperform Growth Stocks?” CBS MoneyWatch columnist Larry Swedroe explains: “Value companies are typically more leveraged (have higher debt-to-equity ratios); have higher operating leverage (making them more susceptible to recessions); have higher volatility of dividends; and have more ‘irreversible’ capital (more difficulty cutting expenses during recessions).”

A Tale of Behavioral Instincts

There may also be behavioral foibles at play. That is, our basic-survival instincts often play against otherwise well-reasoned financial decisions. As such, the market may favor those who are better at overcoming their impulsive, often damaging gut reactions to breaking news. Once we complete our exploration of market return factors, we’ll explore the fascinating field of behavioral finance in more detail, as this “human factor” contributes significantly to your ultimate success or failure as an evidence-based investor.

Your Take-Home

Factors that figure into market returns may be a result of taking on added risk, avoiding the self-inflicted wounds of behavioral temptations, or (probably) a mix of both. Regardless, existing and unfolding inquiry on market return factors continues to hone our strategies for most effectively capturing expected returns according to your personal goals. The same inquiry continues to identify other promising factors that may help us augment our already strong, evidence-based approach to investing. We will turn to these next.